In Summary:

- Strong retail performance: September’s sector-wide rise in consumer spending signals a positive shift in consumer confidence.

- Macroeconomic boosters: Recent finance announcements strengthen financial security and spending power - potentially amplifying past Q3 spending trends.

- Grocery: Consumer wellbeing continues to drive decisions with Vitality’s partner switch positioning Checkers as stronger than ever.

- Apparel: “More pocket, same mindset”, with value-for-money brands emerging as clear winners in the clothing sector.

September Sector-wide Wins

September 2024 has been a strong month for South African retail, with most sectors experiencing YoY spending growth. When compared to past year’s results however, we see a steep increase in August to September spending.

We dive into the macro factors influencing consumer spending below.

Growth in Spend per Category

SA Optimism on the Rise

News of the South African Reserve Bank initiating its monetary easing cycle with a 25 basis point cut in September has eased the debt burden on consumers and increased their disposable income. This, paired with a three-year low in inflation and September marking the fourth month of consecutive fuel price cuts - has added to the general air of economic optimism in the country.

Other factors, including the strengthening of the Rand against international currencies, has reduced import costs - with the potential to decrease retail prices. Although the effects of this haven’t been seen in the apparel sector yet, the stronger rand has already boosted pharmaceuticals and tech hardware imports.

The new two-pot system however, may have the largest immediate impact on consumer spending. The government has reported that withdrawals have already reached R21 billion, with analysts highlighting that 24% of this has been spent on home and vehicle expenses and a further 11% designated toward day-to-day expenses.

In fact, the Reserve Bank estimates the two-pot system could add 0.1% and 0.3% to GDP growth for the country in 2024 and 2025. A massive boost to SA consumers' pockets, with the potential for an additional R2.3 billion per month in the near future.

Overall, positive economic indicators are boosting consumer confidence and our data suggests these factors have likely boosted retail spending.

Historical Q3 Retail Trends Compared

3-Month Growth in Spend: All Retail Categories

Beyond the above positive macroeconomic factors amplifying historical spend drivers like back-to-school purchases and early holiday preparations, there are some new and interesting dynamics affecting purchase behaviour across individual sectors…

Sector Deep Dive: Uneven Growth & Shifting Dynamics

In terms of overall Grocery performance, Checkers (17%) and Woolworths (6%) both reported strong individual YoY growth in September, outpacing the larger retail sector (3% growth). Checkers’ growing presence has been further strengthened with its takeover of vacated Pick n Pay locations, only reinforcing its market position.

Despite Pick n Pay showing a minor recovery (-13% YoY in August to -12% YoY in September), the retailer continues its downward trend, potentially marred by store closures and shrinking market share. Despite this, we are not naive to think things can’t change in the moment - time will tell if Pick n Pay is merely lying low or preparing for its moment of opportunity.

Consumer Vitality Shifts Gears

In recent years, a growing trend towards healthy living has reshaped consumer behaviour, and it's no surprise that Checkers has been quick to capitalise on the movement. As people have become more health-conscious, the demand for premium, healthy groceries has risen, pushing brands to cater to this market shift.

Checkers, following Woolworths, have stepped up to meet this demand. Discovery Vitality is pivoting to consumer preferences (and potentially Shoprite Holding’s strong growth outlook) by opening its doors to its newest Vitality points partner.

Discovery’s new partnership with Checkers from 1 September however, means that Pick n Pay is out. A decade-long relationship has seemingly ended, highlighting a shift towards top-of-mind brands whose performance secures consumer loyalty. This decision, along with Woolworths retaining its Vitality Healthy Food partnership, signals that the brands have become the go-to for health-focused shoppers.

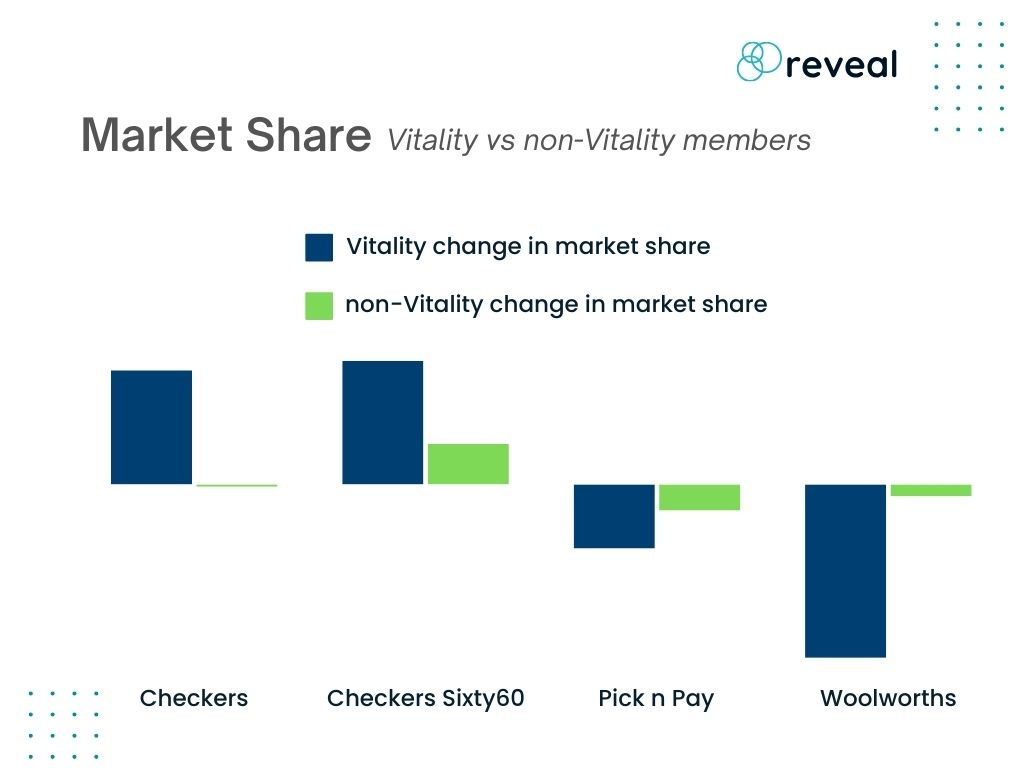

The below graph shows the August to September MoM market share change for Vitality vs Non-Vitality Members:

Who packs the grocery punch?

When we break down Groceries’ market share by number of customers, overall spending, and the number of purchases customers make, it becomes clear that Checkers has an edge. Even though Pick n Pay shoppers tended to spend more per shop, Checkers made up for it by having more customers and a higher number of transactions.

In terms of in-store vs online spending, data shows that online shoppers seem to prefer buying online rather than buying in-store.

Consumer spending for Woolworths also reveals some interesting insights: despite the retailer only holding a small slice of the groceries market “pie”, Woolworths online shoppers had the largest basket size - suggesting that a strategy to direct its customers online would be to the retailer’s advantage.

Not to forget Checkers’ Sixty60, the app has captured a sizable portion of the market, accounting for more than half of Checkers' in-store sales. It also has the highest number of transactions per customer, with shoppers spending just a bit more per online order when compared to those visiting physical stores.

Apparel Sector Spending

Closing off with Apparel, we’re seeing notable shifts. The sector is making a slow comeback. Traditional Clothing’s market share has grown from 82.8% in August to 83.2% while the Footwear category, although the smallest, has increased its share from 5.4% to 5.8%. The Sports and Outdoor category, however, has taken a hit, dropping from 11.8% to 11% despite the warmer weather.

These sector shifts suggest that consumers are reassessing their spending priorities, focusing more on the essentials rather than speciality items like sports gear.

This could indicate that South African shoppers may still be cautious despite the government’s latest announcements.

Merchant breakdown: Checkers goes for Checkmate

The merchant with the strongest September growth has been the most surprising. Pep has emerged with 20% YoY growth, suggesting that value-focused retailers are benefiting from price-conscious customers. It remains to be seen if the introduction of the two-pot retirement system could further drive spending at retailers like Pep, as consumers seek value-for-money items that can stretch their money further.

Not to be stopped, however, Checkers has dived into the Apparel sector. UNIQ has reported impressive YoY growth (73%), despite being a newer retail player. The brand’s growth potential is significant – with transactions increasing and an opportunity to grow basket-size value.

Despite earlier losses, Pick n Pay is holding its ground in Apparel, showing stronger growth than competitors like Ackermans and CottonOn. It’s unlikely that news of Checkers’ wins is driving store traffic, Pick n Pay’s retail department is doing something well amidst its broader challenges in the market.

Looking Ahead: Black Friday and Beyond

With Black Friday on the horizon, retailers are gearing up for one of the year's most significant shopping events. The current positive economic sentiment sets a promising stage, but competition is fiercer than ever.

You can find our 2023 report on last year’s Black Friday retail results by clicking the link. Should you wish to add a competitive edge to your 2024 Black Friday strategy, contact us to pre-purchase our October report and insights round-up now.